Here are some great links making the case that monetary financing for public spending (money printing) is not inherently inflationary and that resistance to its use is purely an ideological choice:

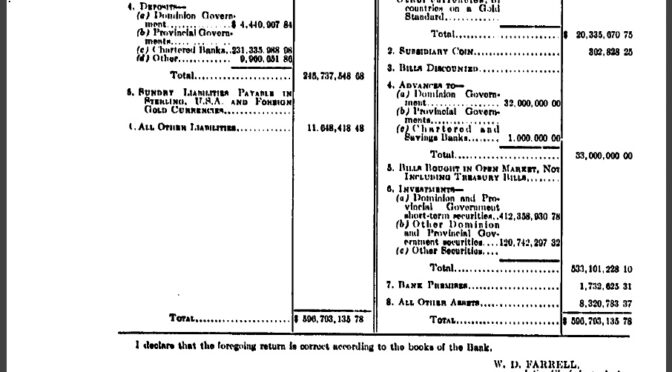

There is much contention surrounding the history of the Bank of Canada making advances to the federal government and provinces. Some claim it never happened, that although there were provisions in the Bank of Canada Act (article 18 (i) and (j)) for advances, this provision was never used. That is incorrect, it was indeed used, multiple times. The reason it took so long to confirm this is because the information was not on the Stats Canada tables of the Bank of Canada balance sheet (which does not go earlier than 1953), it was buried in the Canada Gazette archives. Below is a chart of every time the BoC made advances to governments, the last being in 1961. As you will see, the BoC had no issue giving its biggest advance for the war effort.

Date

Level of government

Amount

2017 dollars

Per Capita

April 1935

Federal

$3,000,000

$54,000,000

$4.98

June 1935

Federal

$4,301,562

$77,965,811

$7.19

July 1935

Federal

$1,240,625

$22,486,328

$2.07

Aug 1935

Federal

$1,246,563

$22,593,954

$2.08

Sept 1935

Federal

$2,759,375

$50,013,671

$4.61

Oct 1935

Federal

$15,724,750

$285,011,093

$26.28

Nov 1935

Federal

$2,223,375

$40,298,671

$3.72

Dec 1935

Federal

$3,465,812

$62,817,842

$5.79

Jan 1936

Federal

$2,195,875

$38,724,552

$3.54

April 1936

Provincial

$2,000,000

$35,270,000

$3.22

May 1936-Sept 1936

Provincial

$3,000,000

$52,910,000

$4.83

Oct 1936

Provincial

$1,000,000

$17,640,000

$1.61

April 1938

Federal

$7,000,000

$117,120,000

$10.50

Sept 1940

Federal

$32,000,000

$522,000,000

$45.86

Jan 1953

Federal

$15,000,000

$138,830,000

$9.35

Nov 1961

Federal

$9,000,000

$74,810,000

$4.10

If you’d like to see the balance sheets from the Canada Gazette for yourself, check them out here:

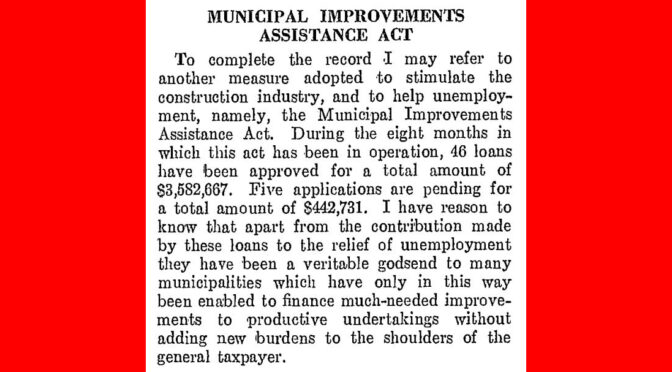

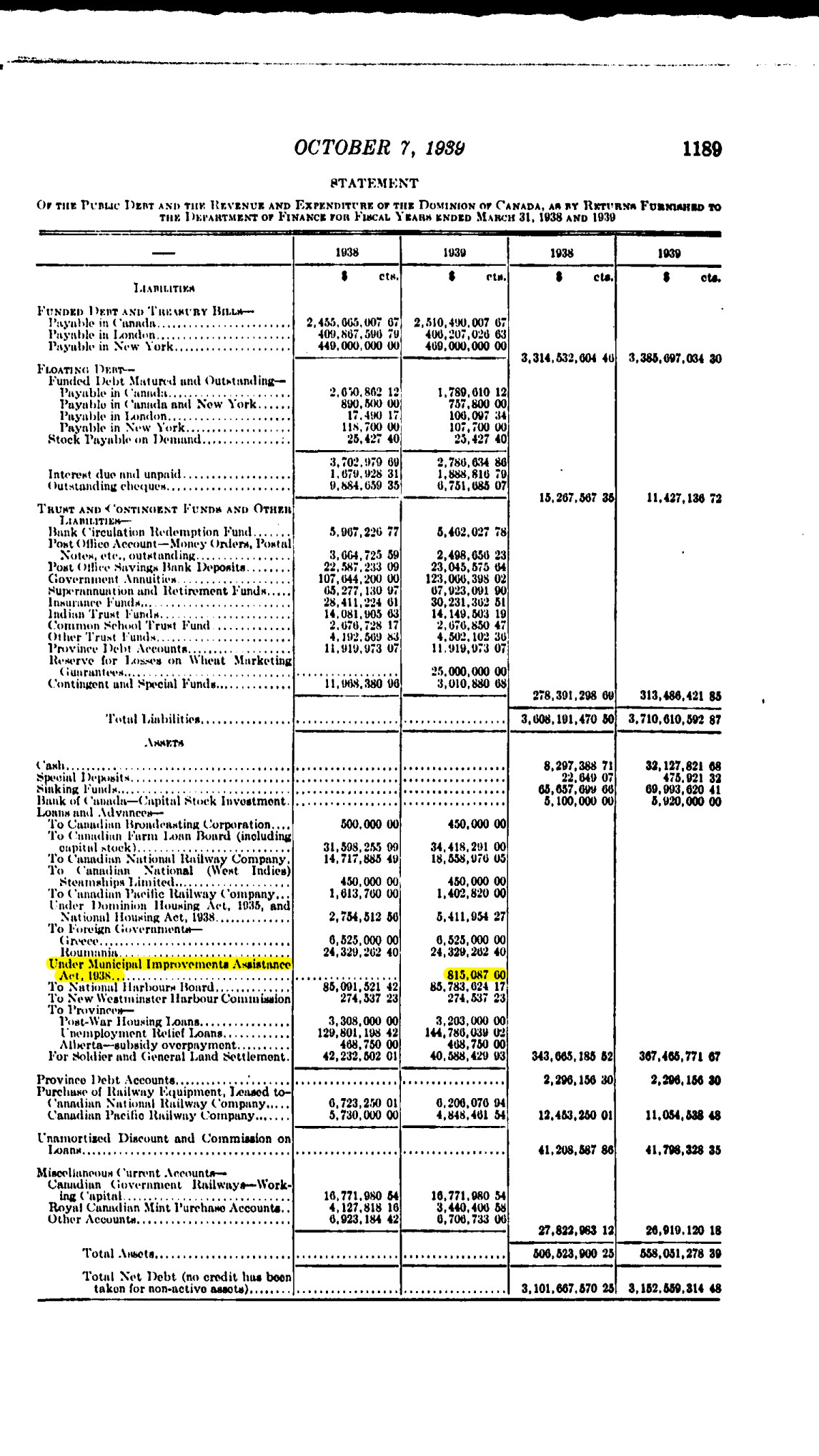

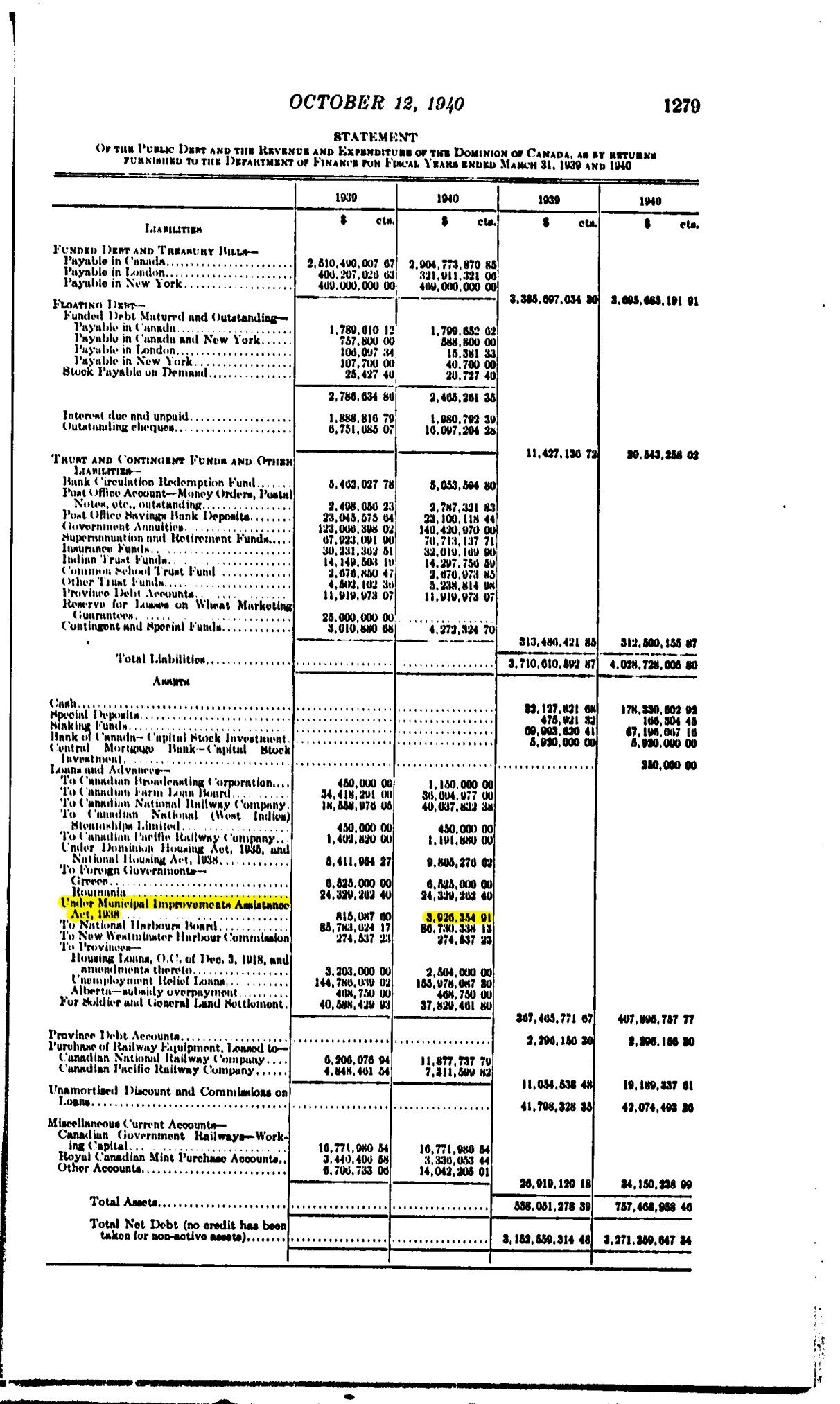

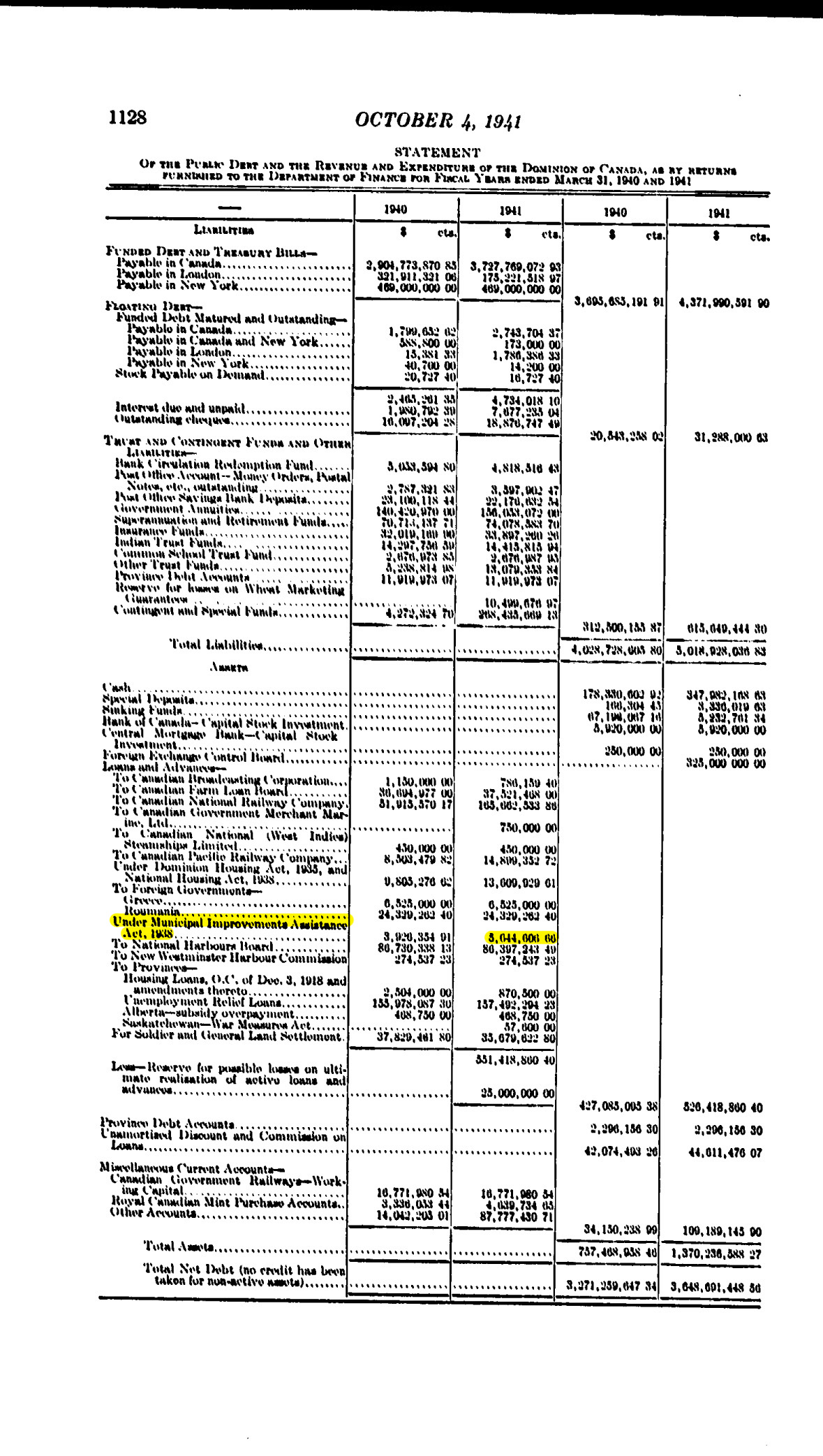

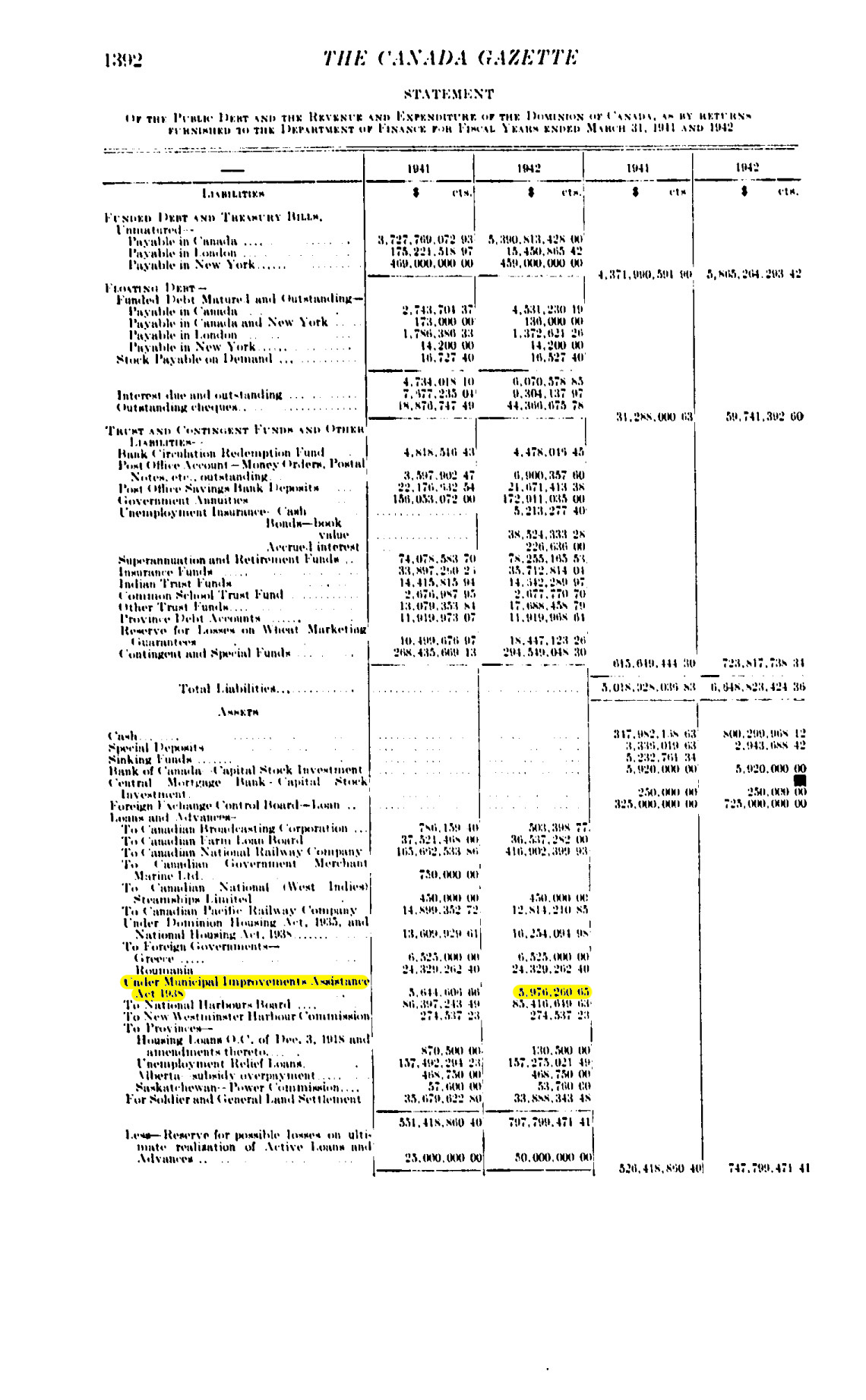

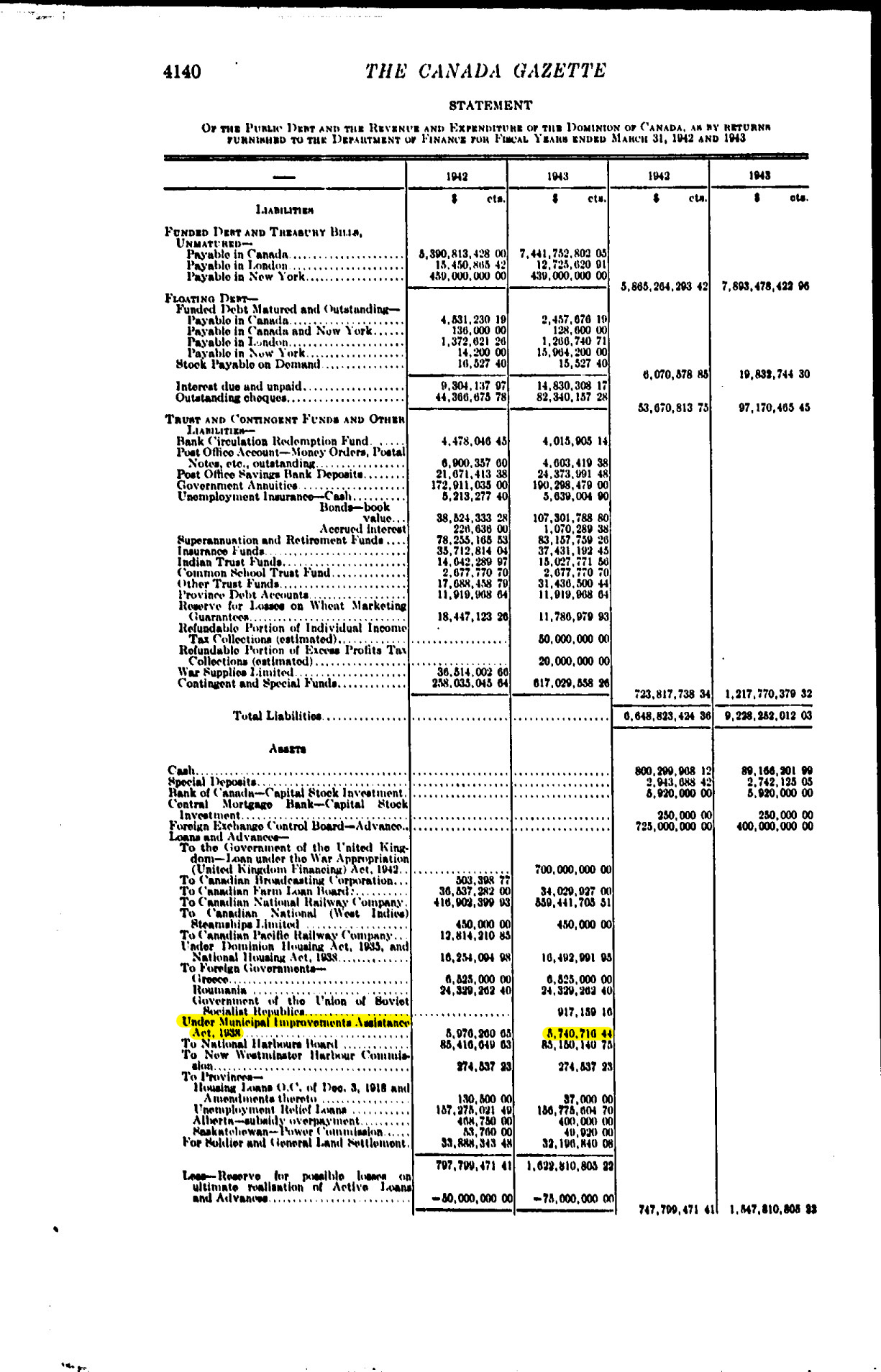

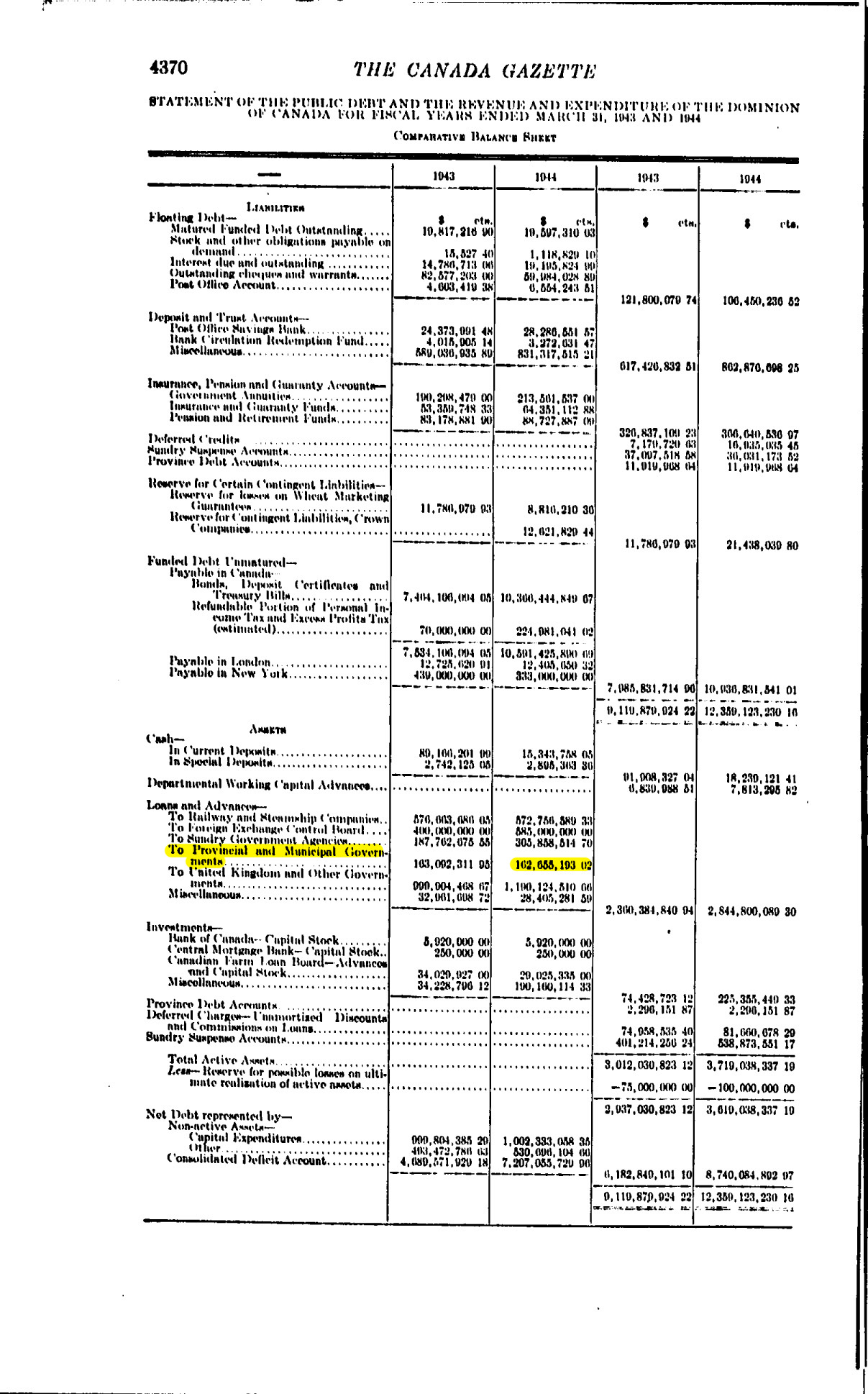

It has been claimed by many that the federal government never made loans directly to cities for infrastructure. This is incorrect, one just needs to dig deep enough into the Canada Gazette archives. There one will find the Municipal Improvements Assistance Act 1938, and the corresponding loan value on the government’s balance sheet. The peak was in 1943 when the total value reached $3,740,716.44. That is $53,644,340.16 in 2017 dollars, at a time when our population was only 11,795,000, making it around $4.50 for every person alive at the time.

After 1943 the government seems to have ended the program, but still has a line about loans and advances to provincial and municipal government, which continues for years afterwards. Once upon a time federal support of local needs was much higher. The full text of the Municipal Improvements Assistance Act is here:

Here’s a quote from 1939 about the good the Act was doing:

“MUNICIPAL IMPROVEMENTS ASSISTANCE ACT

To complete the record I may refer to another measure adopted to stimulate the construction industry, and to help unemployment, namely, the Municipal Improvements Assistance Act. During the eight months in which this act has been in operation, 46 loans have been approved for a total amount of $3,582,667. Five applications are pending for a total amount of $442,731. I have reason to know that apart from the contribution made by these loans to the relief of unemployment they have been a veritable godsend to many municipalities which have only in this way been enabled to finance much-needed improvements to productive undertakings without adding new burdens to

the shoulders of the general taxpayer.”

“34. Under the Municipal Improvements Assistance Act, 1938, the Government approved loans prior to March 31, 1939, amounting to $3,143,000 to municipalities to enable them to finance the construction of municipal self-liquidating projects. As at March 31, 1939, the amount actually paid out on such loans was $815,000. These loans bear interest at the rate of 2% per annum and are amortized over a period not longer than the estimated useful life of the project. The province in which the municipality is located is required to guarantee the payments of interest on and amortization of any such loan.”

It can be pretty difficult digging through old Canada Gazettes to find the Bank of Canada balance sheet information prior to where Stats Canada cuts it off. So we;ve made it easy by putting it all in one document.

The Right Honourable Justin Trudeau, P.C., M.P., Prime Minister of Canada

The Honourable Bill Morneau, P.C., Minister of Finance

Mr.

Nathaniel Erskine-Smith, M.P., House of Commons

Dear Prime

Minister, Minister, and Mr. Erskine-Smith,

Last year an e-petition was submitted to the government requesting the Bank of Canada fulfill its stated role “to promote the economic and financial welfare of Canada”, by returning to previous levels of monetary financing and economic activity[1], as opposed to only focusing on inflation through the blunt and indirect instrument of influencing short-term interest rates in overnight markets.

Minister

Morneau’s response to the petition was troubling, as it cites disproven

assumptions about inflation that Canada’s own history belies. Empirical

evidence shows higher levels of federal monetary financing did not affect

inflation in Canada[2]. Careful analyses of instances of

hyperinflation by institutions like the IMF have proven public money creation

alone is never the culprit, but rather currency speculation, corruption, a poor

understanding of monetary policy and economics, and market forces are of

greater influence[3].

Claiming government monetary

financing is inflationary ignores that private bank money creation dwarfs

government money creation at approximately 97%[4] of our money supply created as

debt with interest attached[5]. It is their loans and credit that have caused

consumer debt rise to nearly 170% of average income and over 100% of GDP[6], while also inflating

asset prices resulting in the soaring housing prices in Toronto and Vancouver[7]. The elimination of reserve requirements at

the BoC in 1991, replaced by the amorphous and ephemeral capital requirements,

ensured what little control over the money supply the BoC had was gone[8]. Also disproving the notion is that the

massive amounts of QE injected into various economies after the ‘08 crisis were

not inflationary to consumer prices either (although it did inflate asset

prices)[9]. Simply put, there is no historical or

empirical evidence proving unequivocally an increase in reserves spent into the

economy is inflationary, especially when the BoC pays interest (the deposit

rate) on those reserves. More

importantly, it is not the government spending reserves into the economy that

is inflationary: it is the potential actions

of private banks in response to the reserves.

Even the Fed admits to this[10].

However,

the most alarmingly ironic statements come from our current BoC governor Mr.

Poloz[11]. In selling the notion that a nation with a

public central bank counter-intuitively needs foreign investment to fund public

infrastructure, he then lists two projects, the St. Lawrence Seaway and the

Trans-Canada Highway, which required no foreign investment whatsoever and were

primarily funded through monetary financing using the Bank of Canada. The

St. Lawrence Seaway did not need US investment, in fact, after the US dragged

its heels for too long Canada threatened to go it alone[12],

and the US finally got involved because it would not have a claim to any

revenues if it didn’t share the cost.

Either Mr. Poloz is intentionally misleading the public on this history,

or he is unaware of the history of the institution he is leading.

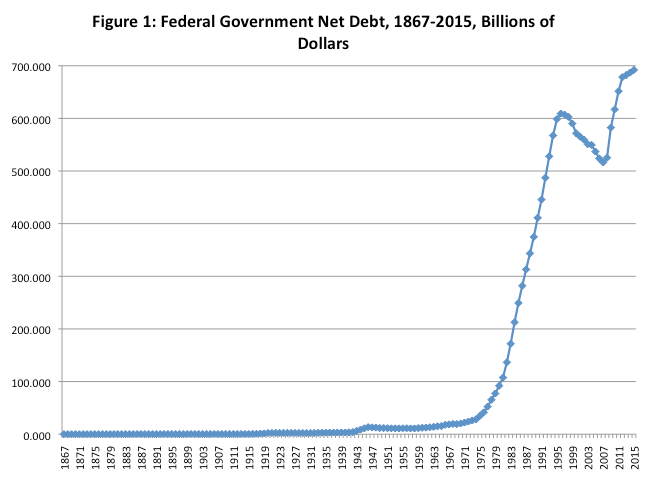

The two most economically beneficial banks in the history of Canada are the Bank of Canada and the Industrial Development Bank (now the BDC). Both had the same auspicious beginnings with a capitalization injection of publicly created funds[13]. At the same time the BoC was nationalized in 1938, the government enacted Bill 143, the Municipal Improvements Assistance Act, which allowed municipalities to borrow directly from the federal government for building municipal infrastructure[14]. The Bank of Canada was once the largest holder of federal debt, using monetary financing to bring us into the unprecedented growth of our golden years in the post-war period, funding many important public infrastructure projects like the St. Lawrence Seaway, Trans Canada Highway, and early parts of the 401 Highway. Even more significant, we had no problem using the BoC to fund our efforts in WWII[15], but somehow we can’t use it for peaceful purposes? As we did until we joined the Bank for International Settlements’ first Basel Committee in 1974[16] and proceeded to adopt monetarism, the now disproven notion that the money supply is the main driver of inflation[17]. The resulting increase in federal debt after 1974 is painfully clear[18], and was a direct and immediate result of these policy changes. The following year the government rescinded Bill 143 in line with the dictates of the BIS. Monetarism forced increased private sector borrowing instead of public money creation, and since then the federal share of the total public debt burden has shifted onto municipalities[19]and is set to further burden cities now that the 2017 budget has reduced their access to federal funding[20].

Let’s say

the government needs to build $1 billion in new infrastructure. It can

either:

– create

the money with the Bank of Canada

OR

– borrow

the funds selling bonds in capital markets

Either

way, $1 billion is spent on public goods, it will have the same result

economically and socially and create the exact same number of jobs and

result in the same physical asset[21], it’s just in the latter option

it needs to be paid back with higher interest than the deposit rate at the BoC. The way our monetary system is constructed

there is no such thing as “interest-free money creation” unless printing cash

or minting coin, because when the government spends money into the economy it

shifts reserves from the Receiver General’s account at the BoC to a private

bank’s account at the BoC, on which the BoC must pay the deposit rate (.25%

less than the target for the overnight rate).

However, the deposit rate is always less than what we pay in interest on

our bonds, else it would incentivize banks to hold more reserves, which in a 0%

reserve requirement environment they do not want to do. The point is, even with the deposit rate on

reserves, the interest paid is cheaper when the BoC creates the money for the

government than when it gets the money from banks’ purchases of bonds.

It is most worrying to hear Prime

Minister Trudeau speak to business audiences wooing them with promises of high

returns with an unnecessary Canada Infrastructure Bank[22], when we already have one that

does not require private investors in the Bank of Canada. The greatest concern of all however comes

from the government’s admission, allowance, and dismissal of the obvious

conflict of interest in allowing a council heavily tilted in favour of big

business interests, representatives from BlackRock (the world’s largest asset

manager) and McKinsey & Co., to devise the plans for the infrastructure

bank that will facilitate the high returns on their investments[23]. Despite the clear conflict, no disclosures

were made and no one recused themselves for any of the council decisions. The government worked for months with these

advisers to prepare for the closed door meeting, organized by BlackRock,

between Prime Minister Trudeau and institutional investors. BlackRock even tailored and vetted the Infrastructure

Minister’s presentation to ensure it was what investors wanted to hear. Furthering the conflict of interest is

Michael Sabia, the president of the Caisse who wants $1.3 billion from Ottawa

for light rail, leading policy discussions on the CIB as a member of Minister

Morneau’s Advisory Council on Economic Growth.

How are Canadians to have faith in a bank structured by the very players

that will profit from it?

The manner

in which the infrastructure bank was presented in legislation does little to

inspire faith in it either. Following in Harper’s tradition the CIB was

jammed into the undemocratic omnibus Bill C-44, which had debate stifled[24],

and which even the Senate is considering severing into separate legislation[25],

as it should be for such an important change to our system. Even a KPMG report for Infrastructure Canada

itself calls for caution and not to rush in before more impacts can be

considered[26].

With our

debt as high as it is (over $1 trillion and counting[27]) and inequality worsening[28], why would we make it

worse promising above average returns and monetizing public infrastructure into

a revenue stream for private investors? Even without public money creation, we can

use traditional bond issues at a lower rate than investors would expect from an

infrastructure bank[29]. The proposed infrastructure bank is a huge

deviation from the Liberal election platform to “use its strong credit

rating and lending authority to make it easier and more affordable for

municipalities to build the projects their communities need.”[30] Multiple studies from around the world

have proven that using private investment to build assets, for example P3s,

costs the public more money, as evidenced by Ontario’s Auditor General[31] and the reversal of

privatizations in Europe[32].

Are you suggesting an

infrastructure bank to build infrastructure or to provide a new revenue

stream for large institutional investors? How exactly are we supposed to

pay back investors? Are you planning to

saddle the new infrastructure with user fees so they become an ongoing revenue

stream? Why do documents show the

government plans to take on more risk to ensure investors get paid first, and

the government last[33]? How much more debt will tax payers be on the

hook for? We already made our debt worse

when in February this year the BoC reduced its automatic minimum purchase of

government bonds from 15% to 14%, increasing our debt burden for no apparent

reason except perhaps to increase the available general collateral in overnight

markets[34]. Harper’s first budget in a majority cranked

the rate up to 20% to suit his needs, the BoC market notice makes clear it was

done “to

accommodate the planned increase in government deposits held at the Bank of

Canada associated with the Government of Canada’s plan announced in the June 2011 budget

to increase its prudential liquidity over the next 3 fiscal years”3. Not the BoC’s plan, the Government of

Canada’s plan, so why can’t we do the same?

The BoC is not autonomous; the disagreement with Governor Coyne that

necessitated an additional clause in the BoC Act proves that[35], as does the

disagreements with Governor Crow that led to him not being renewed for another

term[36].

We don’t need to be a source of

unearned income for investment funds, and we don’t need to sell off public

assets. These are capital assets for which “the cost of acquiring fixed assets is treated as expenditure at the time

of acquisition”[37] instead of being

depreciated over the life of the asset the way private companies can. That capital cost is also is accounted for in

the same budget as the operating budget providing services, unlike

municipalities’ ability to separate capital and operating expenditures[38], the net effect making

deficits appear worse than they are. If

we really need money we’re not willing to create ourselves we should be going

after the billions in tax avoidance and evasion and closing the loopholes that

allow it[39]. We don’t even attempt to measure the tax gap

in Canada[40]. Or consider raising corporate tax rates, as

Canada itself has become a tax haven as evidenced by Burger King’s acquisition

of Tim Horton’s[41],

while corporations sit on billions in “dead money”[42], and Canada has now hit

an unenviable milestone, for the first time ever getting more tax revenue from

people than from businesses[43].

We need to

provide the public with the infrastructure and services needed to ensure a high

standard of living befitting a country of our wealth. Deficits are mere

accounting, and recent economic studies have proven that austerity

shrinks economies and deficit spending grows them[44].

I hope you let evidence and history, and not the specious assumptions

espoused by neoliberal institutions like BlackRock, McKinsey & Co, the

London School of Economics, and the private banking community, guide you to the

conclusion that we already have the

ultimate driver of prosperity and growth: The Bank of Canada.

[2] Figure 1: Monetary financing and inflation in Canada,

1958–2012 “Is Monetary Financing

Inflationary? A Case Study of the

Canadian Economy, 1935-1975” by Josh Ryan-Collins http://www.levyinstitute.org/pubs/wp_848.pdf

[10] “What potentially matters about

high excess reserves is that they provide a means by which decisions made

by banks—not

those made by the monetary authority, the Federal Reserve System—could increase

inflation-inducing liquidity dramatically and quickly.”

[13]“the Prime Minister, as a reflationary

measure, introduced legislation calling for an expenditure of $39 million on

public works to be financed by an expansion of the note issue” from

“The Bank of Canada: Origins and Early

History” by George S. Watts

“the Bank of Canada subscribed for the full initial

stock issue of $25 million and as funds were required drew it down and paid for

it. By starting off with only equity

money and no borrowed funds, the new Bank (IDB) was to have a favourable start

and develop some strength and attractiveness in its operating record before it

should have to borrow and pay interest.” From “The

IDB: A History of Canada’s Industrial

Development Bank” by E. Ritchie Clark. (for

context, that is $652 million and $418 million respectively in today’s dollars)

[14] “This Bill authorizes the Minister

of Finance, with the approval of the Governor in Council, to enter into

agreements to make loans to municipalities to enable them to pay the whole or

part of the cost of constructing or making extension, or improvements to or

renewals of a municipal waterworks system, gas plant, electric light system or

any other self-liquidating project.”

[15]“During the war period, $517.8

million of securities were bought directly from the government with newly created central bank money

and by converting numerous maturing securities into new Government of Canada issues

(Neufeld 1958a, 145; Mcivor 1958, 174). As Plumptre (1941, 155–56) remarks, the effect of

this increase in note issue was to provide “a sort of interest-free loan to the Government

through the medium of the Bank of Canada.” The Bank issued the notes at virtually zero

cost to itself, whilst the profits paid to it by the government for holding government debt were all paid back

to government which owned all of its stock.”

[21]“If a loan

funds the building of a house, or a railway or a broadband network, it is

creating a productive asset. A productive asset creates value over many years,

providing a continuous flow of increased products and services over time. Money

spent on such an asset should thus be able to be absorbed in to the economy

without creating inflation.”http://b.3cdn.net/nefoundation/e79789e1e31f261e95_ypm6b49z7.pdf

[29]“There’s

no shortage of low-cost public financing available to Canadian governments.

Ottawa can now borrow at 0.6 per cent over a year and issue 30-year bonds at

1.8 per cent, with provinces a percentage point higher. Long-term borrowing

rates have never been this low. Meanwhile large private infrastructure

investors expect ‘stable, predictable returns in the 7 to 9 per cent

range’…It doesn’t take an economist to understand it makes no sense to

finance projects at seven to nine per cent when you can do so at two per

cent.”https://canadians.org/blog/trudeau-government-announces-privatization-bank

“This argument doesn’t hold up. Borrowing money is

largely a balance sheet transaction, and if it’s used to invest in

infrastructure there will be assets to match these liabilities for many years

to come,” the report states. Further, they note that Canada has the lowest net

debt-to-GDP ratio of the Group of Seven countries by far.

“The case for establishing the CIB is not compelling,

as it has the potential to increase overall costs to taxpayers while

privatizing the most high-return, low-risk infrastructure assets.”

[35]“Minister’s directive

(2) If, notwithstanding the consultations provided for in subsection (1),

there should emerge a difference of opinion between the Minister and the Bank

concerning the monetary policy to be followed, the Minister may, after consultation

with the Governor and with the approval of the Governor in Council, give to the

Governor a written directive concerning monetary policy, in specific terms and

applicable for a specified period, and the Bank shall comply with that

directive.” http://laws-lois.justice.gc.ca/eng/acts/B-2/FullText.html

[36]“This will mean discarding the polite

fiction that the Bank has any real say over, and therefore responsibility for,

monetary policy formulation – however convenient that story may be for the

government and however flattering the Bank of Canada may find it.” From “Making Money” by John Crow

[38]“An Ontario

municipality may issue long-term debt only for capital purposes and cannot

borrow for operations… Repayment of

municipal debt is amortized over the term of the debenture with regular

contributions being made to the sinking fund.”

[44] “Since the global turn to austerity in 2010, every country

that introduced significant austerity has seen its economy suffer, with the

depth of the suffering closely related to the harshness of the austerity… Meanwhile, all of the economic research that

allegedly supported the austerity push has been discredited… An economy that is depressed even with zero

interest rates is, in effect, an economy in which the public is trying to save

more than businesses are willing to invest. In such an economy the government

does everyone a service by running deficits and giving frustrated savers a

chance to put their money to work. Nor does this borrowing compete with private

investment. An economy where interest rates cannot go any lower is an economy

awash in desired saving with no place to go, and deficit spending that expands

the economy is, if anything, likely to lead to higher private investment than

would otherwise materialise.” “The

Austerity Delusion” by Paul Krugman https://www.theguardian.com/business/ng-interactive/2015/apr/29/the-austerity-delusion

The time had finally come for me to really understand it. I started by researching blockchain, and then started in on Bitcoin. It always seemed a bit fishy to me, something never sat right and so I avoided it. Until now.

Blockchain is an interesting technology, seeming to democratize file storage and reduce system vulnerability to hacks and other cyber attacks. And it’s supposed to be very anonymous, at least in terms of Bitcoin. The first site I researched made blockchain sound like a fortress of privacy impenetrable to attack and manipulation. But what little I knew of Bitcoin always had me doubtful, knowing all I do about banking, finance, and monetary theory.

Like mining bitcoins. It can only be done with a computer devoted solely to doing the complex calculations to maintain the blockchain, and then the miner is rewarded. This automatically gives an advantage to people with the means to devote farms of computers to doing nothing but mining bitcoins, not terribly fair nor democratic. Money creation in bitcoin is not controlled by the needs of government, it is inflexible and therefore cannot expand and contract with the needs of the economy. Bitcoin miners become the new bankers, extracting a form of “interest” for doing the “mining”. Which they don’t do, their computers do, they just need money to buy such a computer.

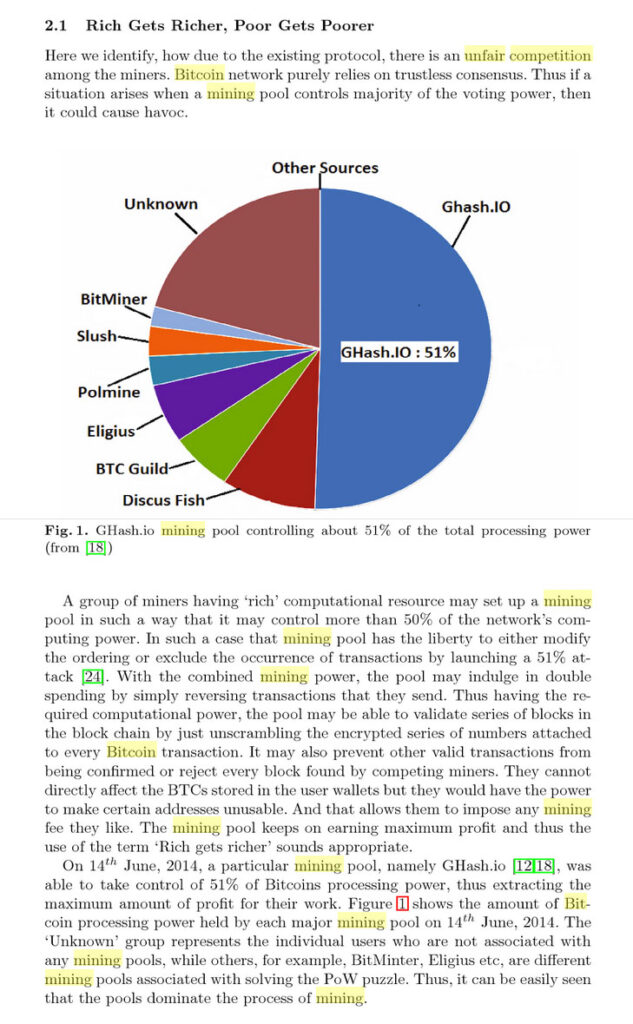

As I researched further I found there are of course scams and imbalances. Massive farms can dominate the network and start dictating the flow of information. A few years ago a company got 51% of the network, and currently two Chinese companies control over 50%. When a nation notorious for control over commercial enterprise starts getting control over a global currency there is a BIG problem. There are other tricks too, to ensure your computer gets ahead in calculating the next few blocks.

It was also interesting to find bitcoin is quite political, beloved by Libertarians for its anonymity and supposed democratization of money. It has a darker side to that anonymity, criminals have been trading in bitcoins to keep their transactions secret.

But now it has been revealed that bitcoins can be traced back to an IP address! So when push comes to shove it’s not as anonymous as everyone thinks and criminals are being busted. Not to mention the records of bitcoin in blockchain means every single bitcoin can be traced to its original miner.

Bitcoin mining is also an incredible waste of resources. The computers necessary to mine bitcoins are expensive and run hot, and companies are devoting massive amounts of hardware and energy into “mining” a digital currency. Seems a lot of that could be better spent doing something productive.

Add to this that it seems the blockchain is hitting limitations due to its increasing size, and that mining for new bitcoins takes more and more computational power as the chain gets longer, and soon bitcoin may have hit its maximum output.

In the end, as far as a monetary instrument, bitcoin fails on a number of levels. First and foremost, its supply cannot be adjusted for the needs of the economy, there is no way to use some of the stabilizers of monetary policy the government uses to ensure a stable currency and manageable inflation. Second, it is unfairly created by people with the resources to buy and power a computer designed solely for bitcoin mining, it has no other purpose. Lastly, it is vulnerable to attack and susceptible to manipulation. Hackers or powerful companies cannot easily hack or take control of our money supply or bank records currently, while bitcoin, especially being less regulated, is open for taking advantage.

Ever since the Toronto Region Board of Trade’s 2013 report on revenue tools for the city, figuring out how to raise more money for transit in Toronto has been a contentious issue. Road tolls come with a host of issues, primarily new administration and expensive infrastructure that other solutions do not require. Also, the last 40 years in Canada has seen the tax burden shift from the bulk being on businesses to being shouldered by residents, and this imbalance is leading to increasing inequality. This report offers alternative revenue sources, most of which have not been considered:

Reinstate the Vehicle Registration Tax, but based on a formula taking into account gas mileage, number of drivers, number of dependents, and number of vehicles per household

Empower TPA officers to start fining illegal vehicle idling

Reinstate the Business Occupancy Tax for financial institutions

Introduce a parking lot levy, especially for malls and office towers

Eliminate the Commercial Property Vacancy Rebate

Halt the reduction of tax rates on Commercial, Industrial, and Multi-residential property tax rates

Increase property taxes on Commercial General class buildings

Create a new class of Residential property tax for houses over $1 million

Ask the federal government to purchase our debt and fund capital projects with the Bank of Canada

Reinstate the Vehicle Registration Tax based on a progressive formula

The Vehicle Registration Tax was a flat fee per vehicle conveniently collected for the city by the province when people renewed their license plates. But being a flat fee it was not progressive; also it exempted commercial, historic, and a few other classes of vehicles. In this day and age of climate change and reducing carbon emissions, a vehicle tax that funds transit is a perfect solution as a city carbon tax of sorts, shifting money from carbon intensive users to fund carbon reducing measures like public transit.

Unlike the former personal vehicle tax, this is based on a formula taking into account gas mileage, number of dependents, number of drivers, and the number of vehicles at the same address. It calculates as follows:

((1/gas mileage [miles per gallon])*1100/(# of dependents+1)/(# of drivers/# of vehicles))

See the accompanying excel sheet to put the formula in action. Under this formula a single person driving a Ferrari would pay $84.62 a year, while a parent of 3 sharing a 2015 Nissan minivan with their spouse would pay $5.73. This formula can be applied to motorcycles as is, a nominal fee could be made for electric cars, maybe $5/year. This tax should be applicable to commercial, historic, and other vehicles that were previously exempt, but perhaps under flat fees according to the class of vehicle (ie. cube van vs 18-wheeler). Not only does this open up a larger revenue base, but with more total vehicles qualifying the tax per vehicle could be reduced overall.

The only catch is verifying how many dependents, it could be that is done with trust under a penalty for false information. The only other document necessary is a list of the gas mileage of vehicles, but this information can easily be found online.

Without stats on everyone’s car in the city it’s impossible to tell how much revenue this would bring in, but the formula can easily be adjusted to bring in more or less. The VRT used to bring in $64 million per year, and it is easy to implement as the Province collected all the fees for the City at the time of vehicle license renewal. This is why it is favourable, as it requires little expense to implement and requires no new infrastructure or disruption of roads.

Empower TPA officers to start fining illegal vehicle idling

Illegal vehicle idling is rampant in this city. At any given time from 9am-9pm major avenues in any given neighbourhood have dozens of people idling in their cars while engaged in their smartphones. For years, despite a growing number of complaints to the city’s idling complaint hotline, the city has chosen to take an educational approach rather than a punitive one. This has resulted in no behaviour changes. Commercial vehicles are no better, from delivery vehicles leaving the engine going while they deliver, to construction vehicles left running all day whether they are being used or not, and the worst offender: taxis waiting for their next fare. I have personally confronted many instances of illegal idling behaviour and am intimately aware of the attitudes and ignorance surrounding the issue. Many people still think the idling limit is three minutes and has temperature exemptions. In combatting climate change and reducing carbon emissions the city could reduce emissions by a few percent merely by cracking down on illegal idlers, all while bringing in new revenue that could be considered a municipal carbon fine.

This revenue would likely reduce over time, as behaviour changes, but it would be a fresh injection of money for the first few years, and more importantly, will change habits that are contributing to climate change. I’ve spoken to the city about what it would take to empower TPA officers to ticket for idling, but it’s not yet clear how many departments would need to agree. A parked car doesn’t pollute and can’t hurt anyone, ticketing idling is more beneficial to public health than ticketing parked cars and TPA officers are already perfectly positioned to ticket idlers.

Adjusting Property Taxes:

All of the next options involve tweaking property tax rates for commercial properties. For the first time in 2014 Canada hit a milestone: nearly half of federal government revenue was from personal income taxes.1 With successive corporate tax cuts by the feds and the province the tax burden has shifted onto people more than ever. Inequality is not as bad as the US, but it’s rising at a faster rate.2 This has not led to more secure jobs or increased investment, but rather a glut of billions of dollars of dead money corporations are sitting on.3

Considering these trends it seems counter-intuitive to be lowering commercial property tax rates, especially on larger buildings run by wealthy multinationals. The private sector has been given many breaks the last decade, and it has only starved governments of revenue while enriching corporate coffers and stunting growth. Rent-seeking and speculation in markets to find ever more elusive returns are the new focus, and the real economy is left twisting in the wind.

All this is to say that bowing to the whims of the private sector’s need for profits to satisfy shareholders has not resulted in progress for residents. The scales have become imbalanced and the city can use its power to alleviate some of that imbalance. The reason for bowing to the private sector is usually because we are held hostage, that if we increase the tax burden too much they will up and take their jobs with them. While there is some truth to this, it is an overblown scare tactic. Toronto is Canada’s largest city and financial center, a property tax increase on office towers for example would have to result in many hundreds of millions of dollars of extra burden before a company is willing to up and relocate to somewhere that is not Toronto, which has become harder as Mississauga and Brampton are already built up and there is nowhere else nearby that has an international airport. Our biggest businesses will always stay in Toronto because we also hold them hostage: they can’t go anywhere else in Ontario that has the amenities that Toronto does.

It is time to end the neoliberal policies giving too much favour to the private sector and start looking how they can do more to support the city that makes them their profits. Small increases to non-residential property taxes spread across many sectors and industries can result in hundreds of millions of dollars that will not adversely impact these businesses.

Reinstate the Business Occupancy Tax for financial institutions

Before 1998 Toronto had a business occupancy tax applied to the property taxes of certain types of businesses, like banks and distilleries. Banks create the majority of our money supply (about 96%) with the click of a button when they make loans, banks are literally digital money factories.4 And they are the most profitable and safe businesses in Canada, raking in billions in profit every year.5

If we need money, we should be going where money is made: the banks. They also cannot move their branches, if a local branch leaves a hole in a neighbourhood, its customers are likely to seek out another bank that is local. Competition between banks ensures they will not flee Toronto because of a small increase in property taxes.

Introduce a parking lot levy, especially for malls and office towers

This is not a new idea, but it still seems to be getting ignored. Adding a parking levy to malls would have two effects: bringing in more revenue, and leveling the playing field between malls and main street storefronts where customers have to pay TPA to park on the street. Malls and their customers aren’t going anywhere, business is booming.

A levy based on the square footage of a parking lot could be applied to any parking lot over a certain size.

Eliminate the Commercial Property Vacancy Rebate

The BIAs across the city have been calling for this one for a while. Too many long-time property owners are leaving their commercial storefronts empty because there is no impetus to fill them: they have long since paid their mortgages, have rents from residential units above the storefronts giving them profits, and they get a discount on their property taxes, all while an empty storefront rots below. Commercial rents in some areas of the city are exorbitant simply because landlords can afford to gouge. If they can afford to keep it empty, they can afford to pay full property taxes on it. An even harsher suggestion is that if a landlord can’t fill their commercial space but refuses to lower the rent they should be fined for the empty storefront.

Halt the reduction of tax rates on Commercial, Industrial, and Multi-residential property tax rates

In order to attract and retain business in an environment of competition for the lowest tax rates, the city felt it prudent to incrementally lower non-residential tax rates to a ratio of 2.5 by 2020. Other than the usual favouring of the private sector, there is little purpose changing this ratio serves except to add yet another shift of the tax burden from business onto residents. With the exception of residual commercial class spaces, all other forms of commercial, industrial, and especially multi-residential are not in distress, have plenty of money, and do not need reductions in their taxes. Industrial and multi-residential are again examples of businesses that are trapped, they can’t just up and leave to take their business elsewhere. And reducing the tax rate on new multi-residential is just an incentive to build more, faster, at a cheaper rate. Developers do not need this break nor any incentive to build.

Increase property taxes on Commercial General class buildings

Like the banks, commercial general class buildings have the most to give. They are not struggling institutions in need of tax breaks to survive: they are multi-million dollar enterprises rolling in millions of profits. Mega malls, office towers, sports complexes, all are ripe for giving more back to the city that feeds their profits.

Create a new bracket of Residential property tax for houses over $1 million

Residential property taxes are not at all progressive, it is the same rate whether you own a bungalow in Etobicoke or a mansion in Forest Hill. Just as there are two tax brackets for Residual Commercial, so too should massive homes taking up large tracts of land and requiring more services be required to pay a higher rate.

Ask the federal government to purchase our debt and fund capital projects with the Bank of Canada

We are lucky in Canada to have a publicly owned central bank. The Bank of Canada being sovereign is what allowed us to pull ourselves out of the Great Depression, fund WWII, and build a lot of infrastructure in the 50s and 60s, like the St. Lawrence Seaway and the Trans Canada highway, that ushered Canada into its golden years.6 It is not remotely inflationary to spend government-created money into the economy.

The federal government has full power over the Bank of Canada, and although they like to keep it arms-length, the Minister of Finance holds all the shares and if push comes to shove the Minister can order the Bank to do as the government needs (as happened in the 90’s when BoC Governor John Crow’s obsession with inflation and high interest rates was destroying the economy and exponentially increasing government debt).

When the federal government loans money to itself it pays interest, which goes back to itself, as opposed to selling bonds in private capital markets, where the interest goes to private investors. The federal government also gets a lower interest rate on bonds compared to provinces and municipalities. This begs the question: why can’t the feds use the Bank of Canada to aid struggling municipalities and provinces with their debt load? The short answer is, they can but won’t. The long answer is public money creation does little to increase private profits or give investors a safe place to park their money for a small but safe return (government bonds), and it puts them in direct competition with private banks and their money creation. It is part of the neoliberalism that infected Western governments in the 70s, the focus is on “free” markets, deregulation, and privatization, and that requires the slow and systematic starving of the government and public service. But it doesn’t have to be this way.

There is a growing movement for public money creation across the world. The federal government is in the middle of a lawsuit by the Committee on Monetary and Economic Reform to reinstate the Bank of Canada to the government lending institution it once was before Pierre Trudeau dismantled that function at the behest of private central bankers at the Bank for International Settlements in 1974.7 Councillor Wong-Tam has already called for public banking in Toronto8, and if the city were to officially take such a stance with the feds it would go a long way to sending a strong signal that things aren’t working as they should and a new way needs

to be found.

Conclusions:

Quite simply, the status quo is not working and the needs of Toronto cannot be met or sustained under the current system. The private sector has been given an undue amount of tax breaks from all levels of government, and the result of this neoliberal policy is that all levels of government are now starved for revenue. As these breaks were brought in incrementally, so they can be shifted away incrementally. Canada’s federal corporate tax rate used to be nearly 50%, and our businesses did just fine. It was decades in an environment of neoliberal deregulation, privatization, and downloading of services that brought us to the current crisis. Toronto has never recovered from Harris’ tenure as Premier, the downloading of services created new costs faster than we could find new revenue and we’ve been struggling ever since.

If the city continues on the current path, inequality, poverty, congestion, a transit deficit, and approved but unfunded capital projects will only worsen. The current funding models are just not sustainable, and the private sector has been given too much power to call the shots for their own profits. It’s time for the pendulum to swing the other way, in favour of the public.

My name is Adam Smith, and I’ve been studying banking, finance, monetary theory, and revenue tools for years. When the TRBOT released their 2013 revenue tool study I immediately took an interest as I felt the options were not ideal or equitable enough. I was lucky enough to spend hours discussing some of my options with Richard Joy from the TRBOT. I even created a facebook page about the issue:

I am also a part of COMER – Committee on Monetary and Economic Reform, and I was on the board of the Beach Village BIA for 6 years. Through my work with the BIA I not only know a lot about local businesses and their struggles, but I also know a lot about how the city works and funds programs.

I do not come to these conclusions lightly; they are the culmination of years of research and thought. I’m sure it’s a hard sell to say we need to increase taxes on businesses, but our largest can more than afford it, and with inequality increasing the city will not be economically viable if people can’t afford to be there. The city must take its own steps to rebalance the scales, the province and feds are part of the problem, they created the conditions we struggle under.

Thanks you for reading, please feel free to share this document.

The case for a Near-Winner (Baden-Wurttemberg) Proportional System in Canada

Introduction:

There is one proportional system, from the German state of Baden-Wurttemberg, that should be getting a lot more attention. Baden-Wurttemberg was the first place in the world to use a Mixed Member Proportional electoral system, so it’s only fitting that today they have evolved the best proportional system. In studying electoral reform in Ontario, the Standing Committee on the Legislative Assembly travelled to Stuttgart to observe an election using the Near-Winner Proportional system. In light of how favourable the results were it is strange it has not been given more consideration.

In the Near-Winner Proportional system the voting and ballot are the same as Canada’s first-past-the-post: one vote for one person who will represent one riding. This elects the local direct candidates that represent a specific riding. To achieve proportionality there are local direct seats and regional top-up seats. The percentage of regional top-up seats awarded to each party to make the total seats proportional are determined by the nation-wide popular vote totals, and the regional top-up seats are awarded to the candidates with the most votes who came in second, third, or even fourth place in their riding. Which is why it is called “near-winner”. This way there are no list candidates, every candidate has to run in a riding and was on a ballot somewhere.

Baden-Wurttemberg is only a single state, and the regional top-up seats are divided into 4 regions. In a Canadian model, the regions for regional top-up seats would be the provinces. We start with a regular first-past-the-post election result to determine all the local direct seats and the nation-wide popular vote, and then determine each party’s proportion of regional top-up seats from the nation-wide popular vote. If a party earns regional top-up seats, the seats are awarded to their candidates that got the most votes but did not win a seat. This means some ridings will end up with 2 or possibly 3 MPs, but every riding will have at least 1 local MP, and this is no different than the regional distribution of MPs in a Mixed Member Proportional system.

Advantages over other systems:

A Near-Winner Proportional voting system removes most of the issues with Single Transferable Vote and Mixed Member Proportional systems. The ballot is simple and unchanged from our current ballot, there is no need for party lists or ranking, there is no vote splitting or strategic voting, it is as close to 100% proportional as possible, and independent candidates do not skew the proportional results. It also removes the need for a by-election if a regional top-up seat is vacated mid-term, as the next most popular candidate in that party in that province would be next in line. As the minimum seats for each province apportioned by the Constitution are maintained, implementing this system would not require a change in the Constitution, in fact, it can be instituted with the current 338 ridings.

Drawbacks:

The only drawback to Near-Winner Proportional is there can still be overhang seats, this being less likely in larger provinces with more regional top-up seats and more likely in smaller provinces with less regional top-up seats. Typically an overhang seat is when a party wins more local direct seats than their proportion of the nation-wide popular vote would allow, but it is a slightly different calculation for Canada as we have so many regions with varying quantities of regional top-up seats. Other parliaments like Germany and New Zealand sometimes have variances in the number of seats in their parliament due to overhang votes, so it’s not unheard of to have a shifting number of seats. Any extra seats are removed once a new election starts.

Applying it to Canada:

This system could easily be applied without changing the number of seats or their apportionment per province. Same as the suggestions for Mixed Member Proportional, the riding size for local direct candidates would have to increase to allow for a number of regional top-up seats, but the total number of seats per province could stay the same. There would be a certain number of local direct seats and a certain number of regional top-up seats for each province. The nation-wide popular vote total would determine the number of regional top-up seats awarded to each party, the province-wide popular vote total would determine the distribution of the regional top-up seats, and the winners of the regional top-up seats would be determined by who got the most votes in their province but did not win a seat.

This “near-winner” system would result in some areas having a higher concentration of MPs, but a Mixed Member Proportional system would have the same issue. Regional top-up MPs in a Mixed Member Proportional system are not bound to any specific location for their constituency office within their region, and it is likely they would situate themselves in an area with a higher more concentrated population, an area likely to already have a local direct MP located there.

Many voters overvalue the notion of having a local MP. While it is important to be able to turn to someone who knows your area, by nature very few federal issues are local, they typically affect the whole nation. MPs do their most important work for us in Ottawa, as part of committees or in the House of Commons, not on the ground in their riding. For example, if the Green Party failed to elect any local direct candidates, a Green Party voter in Ontario could still turn to a regional top-up Green Party MP in BC to represent their interests. And empathy is important to consider, just because an MP does not live in a riding does not mean they cannot empathize with that riding’s concerns or are unable to help them. Most problems can be related over telephone or email, a face-to-face meeting is not necessary to get an MP to understand your problem or position.

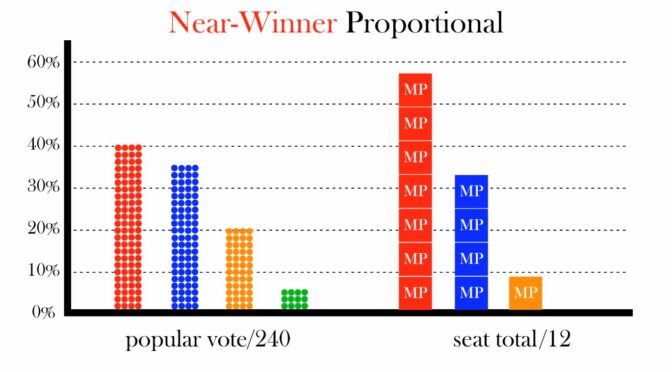

Simulation for a Near-Winner Proportional system using 2015 election results:

The minimum percentage of regional top-up seats necessary to achieve proportionality is 40%, so the number of local direct seats and regional top-up seats for each province would be apportioned from a 60/40 split of the current number of seats per province:

PROVINCE (total seats):

Local Direct Seats (60%):

Regional Top-Up Seats (40%):

ONTARIO (121):

73 local direct

48 regional top-up

QUEBEC (78):

47 local direct

31 regional top-up

BRITISH COLUMBIA (42):

25 local direct

17 regional top-up

ALBERTA (34):

20 local direct

14 regional top-up

MANITOBA (14):

8 local direct

6 regional top-up

SASKATCHEWAN (14):

8 local direct

6 regional top-up

NOVA SCOTIA (11):

7 local direct

4 regional top-up

NEW BRUNSWICK (10):

6 local direct

4 regional top-up

NEWFOUNDLAND & LABRADOR (7):

4 local direct

3 regional top-up

PRINCE EDWARD ISLAND (4):

2 local direct

2 regional top-up

NORTHWEST TERRITORIES (1):

1 local direct

0 regional top-up

YUKON (1):

1 local direct

0 regional top-up

NUNAVUT (1):

1 local direct

0 regional top-up

TOTAL (338):

203 local direct seats

135 regional top-up seats

We use the 2015 election results of the party seat share per province to estimate what the local direct seat share per province would be in a Near-Winner Proportional system. But, with a smaller number of local direct seats, the seat totals and the percentage of seats will be rounded off slightly.

PARTY:PROVINCE:

Liberal

Conservative

NDP

Green

Bloc

ONTARIO:

Current seats 121 (100%):

80 (66%)

33 (27%)

8 (7%)

0

0

Local direct seats 73 (100%):

48 (66%)

20 (27%)

5 (7%)

0

0

QUEBEC:

Current seats 78 (100%):

40 (51%)

12 (15%)

16 (21%)

0

10 (13%)

Local direct seats 47 (100%):

24 (51%)

7 (15%)

10 (21%)

0

6 (13%)

BRITISH COLOMBIA:

Current seats 42 (100%):

17 (40%)

10 (24%)

14 (33%)

1 (2%)

0

Local direct seats 25 (100%):

10 (40%)

6 (24%)

8 (32%)

1 (4%)

0

ALBERTA:

Current seats 34 (100%):

4 (12%)

29 (85%)

1 (3%)

0

0

Local direct seats 20 (100%):

2 (10%)

17 (85%)

1 (5%)

0

0

MANITOBA:

Current seats 14 (100%):

7 (50%)

5 (36%)

2 (14%)

0

0

Local direct seats 8 (100%):

4 (50%)

3 (38%)

1 (12%)

0

0

SASKATCHEWAN:

Current seats 14 (100%):

7 (50%)

5 (36%)

2 (14%)

0

0

Local direct seats 8 (100%):

4 (50%)

3 (38%)

1 (12%)

0

0

NOVA SCOTIA:

Current seats 11 (100%):

11 (100%)

0

0

0

0

Local direct seats 7 (100%):

7 (100%)

0

0

0

0

NEW BRUNSWICK:

Current seats 10 (100%):

10 (100%)

0

0

0

0

Local direct seats 6 (100%):

6 (100%)

0

0

0

0

NEWFOUNDLAND AND LABRADOR:

Current seats 7 (100%):

7 (100%)

0

0

0

0

Local direct seats 4 (100%):

4 (100%)

0

0

0

0

PRINCE EDWARD ISLAND:

Current seats 4 (100%):

4 (100%)

0

0

0

0

Local direct seats 2 (100%):

2 (100%)

0

0

0

0

NORTHWEST TERRITORIES:

1 (100%)

0

0

0

0

YUKON:

1 (100%)

0

0

0

0

NUNAVUT:

1 (100%)

0

0

0

0

TOTAL CURRENT SEATS 338:

184 (54%)

99 (29%)

44 (13%)

1 (0.2%)

10 (3%)

TOTAL DIRECT SEATS 203:

114 (56%)

56 (28%)

26 (13%)

1 (0.4%)

6 (3%)

Now that we have estimates for the local direct seats won by each party in each province, we can calculate the regional top-up seats. There is one catch: votes for independent candidates and very small parties. Most Mixed Member Proportional models have a minimum threshold of vote share for a smaller party to qualify for a regional top-up seat, usually with the reason of preventing fringe parties from getting elected. However this is not democratic. It is my contention that as long as a party gets the minimum nation-wide popular vote for a single seat, that is 0.23% in Canada, it should receive a seat. In our case no independent party reached that threshold, so to calculate each party’s regional top-up seats first we must subtract all independent votes and non-electing party votes from the national totals before calculating each party’s percentage of the nation-wide popular vote. These are the only wasted votes. Fractions of seats are added in order of the largest fraction first until all seats are filled. The formula is:

(Nation-wide popular vote share percentage x 338) – local directs seats = regional top-up seats

Nation-widePopular vote

Local Direct seats won

Regional Top-Up seats added

Totalseats

Proportionof seats

Liberal

39.79%

114

20

134

39.64%

Conservative

32.17%

56

53

109

32.24%

NDP

19.89%

26

41

67

19.82%

Green

3.46%

1

11

12

3.55%

Bloc

4.7%

6

10

16

4.73%

As we can see, the end result of seat proportion almost exactly matches the nation-wide popular vote. The next step is to calculate how many regional top-up seats go to which province. Again, votes for independents or non-elected parties need to be subtracted from the province-wide vote total to get an accurate percentage of the province-wide popular vote per party. Fractions of seats are added in order of the largest fraction first until all seats are filled. The formula is:

(Province-wide popular vote share% x total province seats) – local directs seats = regional top-up seats

Ontario (121):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

44.95%

48

6

44.63%

-0.32%

Conservative

35.37%

20

23

35.54%

+0.17%

NDP

16.81%

5

15

16.53%

-0.28%

Green

2.87%

0

4

3.31%

+0.44%

TOTAL:

73

48

Quebec (78):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

36.16%

24

4

35.9%

-0.26%

Conservative

16.76%

7

6

16.67%

-0.09%

NDP

25.42%

10

10

25.64%

+0.22%

Green

2.26%

0

2

2.56%

+0.3%

Bloc

19.41%

6

9

19.23%

-0.18%

TOTAL:

47

31

British Columbia (42):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

35.34%

10

5

35.71%

+0.37%

Conservative

30.16%

6

7

30.95%

+0.79%

NDP

26.2%

8

3

26.19%

-0.01%

Green

8.3%

1

2

7.14%

-1.16%

TOTAL:

25

17

Alberta (34):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

25%

2

6

23.53%

-1.47%

Conservative

60.63%

17

4

61.76%

+1.13%

NDP

11.85%

1

3

11.76%

-0.09%

Green

2.6%

0

1

2.94%

+0.34%

TOTAL:

20

14

Manitoba (14):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

45.19%

4

2

42.86%

-2.33%

Conservative

37.82%

3

2

35.71%

-2.11%

NDP

13.8%

1

1

14.28%

+0.48%

Green

3.19%

0

1

7.14%

+3.95

TOTAL:

8

6

Saskatchewan (14):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

23.95%

4

0

28.57%

+4.62%

Conservative

48.74%

3

4

50%

+1.26%

NDP

25.21%

1

2

21.43%

-3.78%

Green

2.1%

0

0

0%

-2.1%

TOTAL:

8

6

Nova Scotia (11):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

62.36%

7

0

63.63%

+1.27%

Conservative

17.99%

0

2

18.18%

+0.19%

NDP

16.27%

0

2

18.18%

+1.91

Green

3.38%

0

0

0%

-3.38%

TOTAL:

7

4

New Brunswick (10):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

51.56%

6

0

60%

+8.44%

Conservative

25.38%

0

2

20%

-5.38%

NDP

18.37%

0

2

20%

-1.63%

Green

4.65%

0

0

-4.65%

TOTAL:

6

4

Newfoundland and Labrador (7):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

66.49%

4

0

57.14%

-9.35%

Conservative

10.64%

0

1

14.23%

+3.59

NDP

21.75%

0

2

28.57%

+6.82

Green

1.11%

0

0

0%

-1.11%

TOTAL:

4

3

Prince Edward Island (4):

Popular voteprovince-wide

Local Direct seats won

Regional top-up seats added

Seatpercentage

Seat % – Popular vote difference

Liberal

58.6%

2

0

50%

-8.6%

Conservative

19.38%

0

1

25%

+5.62

NDP

16.06%

0

1

25%

+8.94

Green

6.06%

0

0

0%

-6.06%

TOTAL:

2

2

Inevitably, due the rounding of fractions of percentages and some overhang of Liberal seats, some of the distribution of regional top-up seats when broken down by province do not match the distribution of regional top-up seats calculated for the whole nation. The Liberals have ended up with 3 extra regional top-up seats, the NDP break even, and the Conservatives, Greens, and Bloc are each missing 1. There are three solutions to this:

1. The first solution is to switch some of the regional top-up seats to bring their numbers in line with the calculation of regional top-up seats based on the nation-wide popular vote. The Bloc is easy as they only run in Quebec, so in Quebec the Liberals would lose one regional top-up seat and the Bloc would gain one. Now the Liberals only have two extra seats and the Bloc has all their seats.

After that we look at which provinces have Liberal regional top-up seats available to switch, as you can’t switch local direct seats. From those provinces we look at which ones have the biggest difference between the province-wide popular vote percentage and the final seat percentage. In Manitoba the Conservatives are down -2.11%, so we take away one Liberal regional top-up seat and add one Conservative regional top-up seat. Lastly, the Greens are down -1.16% in British Columbia, so we take away one Liberal regional top-up seat and add one Green regional top-up seat. Now everyone’s seat totals are in proportion to the nation-wide popular vote.

2. The second solution is to add regional top-up seats to compensate. The Conservatives, Greens, and Bloc would each get one extra seat, expanding the House of Commons to 341 seats for that term.

3. The last solution is to do nothing, and accept that while there is a touch of imbalance, it is still a far superior and more proportional result than any other system.

Here are the final proportions of each solution compared to the nation-wide popular vote:

Popular votenation-wide

Solution 1

Solution 2

Solution 3

Seat#

Seat%

Diff.

Seat#

Seat%

Diff.

Seat#

Seat%

Diff.

Liberal

39.79%

134

39.64%

-0.15%

137

40.16%

+0.37%

137

40.53%

+0.74%

Conservative

32.17%

109

32.24%

+0.07%

109

31.96%

-0.21%

108

31.95%

-0.22%

NDP

19.89%

67

19.82%

-0.07%

67

19.65%

-0.24%

67

19.82%

-0.07%

Green

3.46%

12

3.55%

+0.09%

12

3.52%

+0.06%

11

3.25%

-0.21%

Bloc

4.7%

16

4.73%

+0.03%

16

4.69%

-0.01%

15

4.44%

-0.26

Total Seats:

338

341

338

Solution 1 by far achieves the most proportionality, but the switching of regional top-up seats could prove tricky in tighter elections. Solution 2 is less proportional than 1, and requires extra seats, a convention that would be very unfamiliar to Canadians. Solution 3 is the least proportional but is the easiest solution to implement.

The final step is allocating the regional top-up seats to an MP. This is quite simple, we just take the candidates that got the most votes for their party in each province. This is the “near-winner” aspect of the system, the part that ensures every candidate had to run somewhere and is not just on a list.

Conclusions:

After much research and analysis, the Near-Winner Proportional system is superior in every way, and easily applicable to Canada. It’s simplicity at the ballot box and the highly proportional results are its greatest strengths. No matter which version of solution is chosen, the results are still much more equitable than any other system. I hope you agree, I will soon be producing a video animation of this report detailing how it would work. Please give this serious consideration, I have spent many hours studying many systems and once I stumbled upon this one everything clicked.

Who will win the battle for Canada’s future? The pretty boy Disney prince puppet, or the robotic Lego dictator…

For those wishing to delve deeper, we’ve made the Political Junkie Edition, digging up every piece of history when can find showing that the Libs and Cons are each just two sides of the neoliberal coin, both taking turns dismantling Canada for corporate power.

{kind=link}